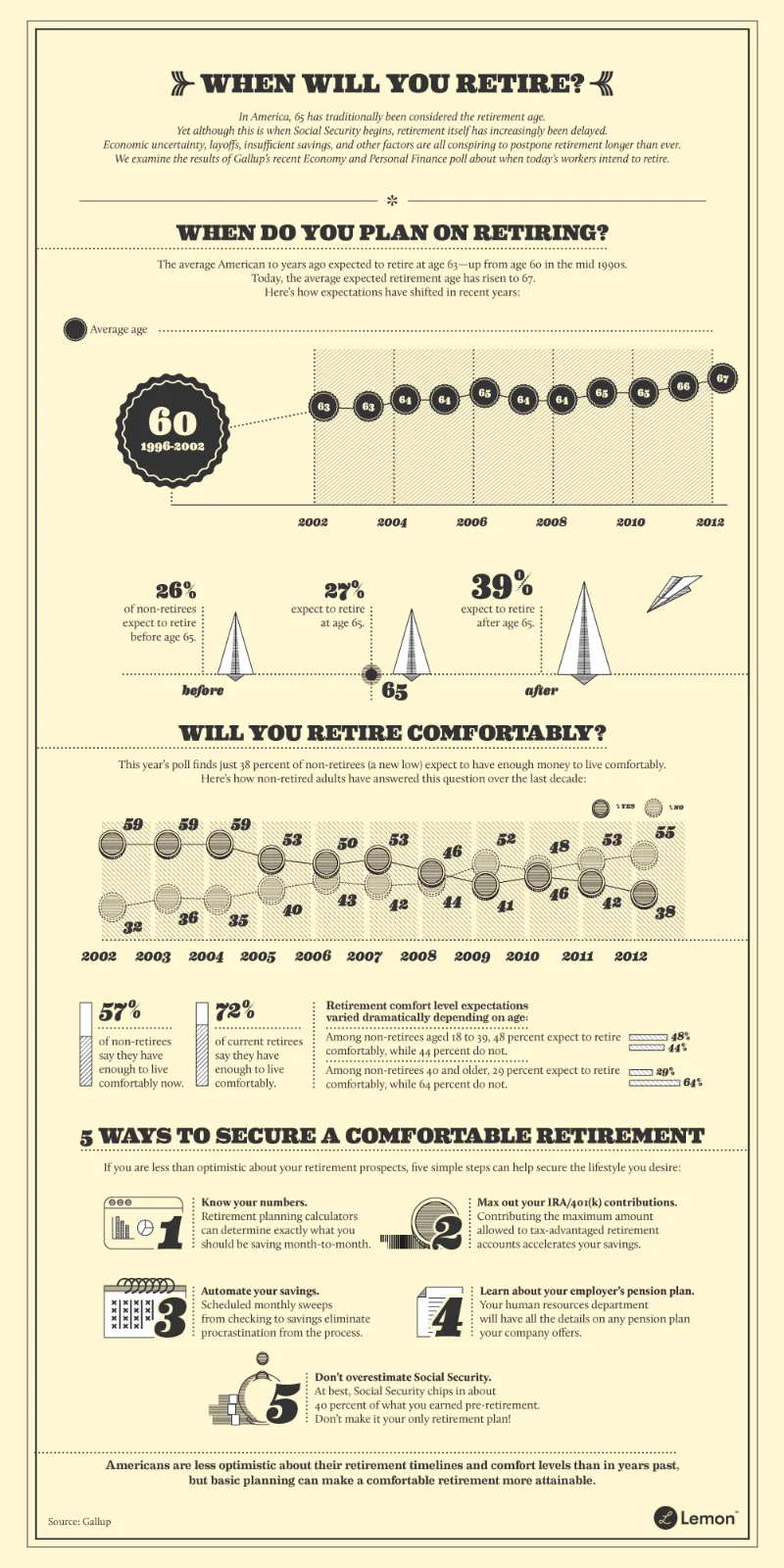

Retirement Age: What It Is vs. Social Security Benefits

The Siren Song of 63

The 2024 MassMutual Retirement Happiness Study has dropped, and the headline is this: 63 is the magic number. Apparently, that’s the “ideal retirement age” according to most American retirees and pre-retirees. Now, I’m all for aspirational thinking, but let’s inject a dose of reality here.

The study also notes that the average retirement age is 62. Conveniently, that's also the earliest age you can start pulling Social Security. But here's the rub: retiring at 62 instead of your full retirement age (which, for many, is 67) means your Social Security benefits could be roughly 30% lower. Thirty percent! That's not a rounding error; that's a significant chunk of change that can make or break your golden years.

And this is the part of the report that I find genuinely puzzling. The same study reveals that 35% of pre-retirees are staring down the barrel of insufficient retirement savings to live comfortably if they retire at their "ideal" age. Furthermore, 34% are legitimately worried they'll outlive their savings, a fear shared by 22% of current retirees. So, we're aiming for this idyllic retirement at 63, knowing full well that a huge percentage of us are financially unprepared. It's like setting a course for a tropical island on a raft made of popsicle sticks.

Is there a disconnect here, or am I missing something? Are people genuinely believing they can retire comfortably at 63 with inadequate savings, or are they simply stating a preference divorced from financial reality? And more importantly, why is 63 the magic number? What makes that particular year so appealing? Is it a health thing? A family milestone? Or just wishful thinking fueled by too many early-bird specials? Most Americans think 63 is the perfect age to retire, but they’re dead wrong. Here’s the big number to bet on - Yahoo Finance

Social Security: The Elephant in the Room

Let's talk about Social Security. In 2022, roughly 16.4 million people were completely dependent on those checks, according to Pew Research Center data. That's a lot of people relying on a system that's increasingly looking shaky. Concerns are mounting that the Social Security trust fund could start running dry as early as 2033.

Think of Social Security like a giant, publicly-funded piggy bank. More people are taking money out (retirees) than are putting money in (the current workforce). The math doesn't lie. And while Congress will likely step in to "fix" things (raise the retirement age further, cut benefits, increase taxes – the usual levers), the uncertainty is enough to give anyone pause.

The study doesn't delve into how pre-retirees plan to bridge the gap between their desired retirement age and their actual financial readiness. Are they banking on a sudden windfall? Planning to work part-time? Relying on family support? Or are they simply hoping for the best and bracing for the worst? The silence is deafening.

Frankly, the whole "ideal retirement age" concept feels a bit… arbitrary. It's a nice thought, but it's detached from the cold, hard realities of savings rates, inflation, and the looming Social Security question mark. Retirement planning isn't about picking a number out of thin air; it's about crunching the numbers, making realistic projections, and adjusting your expectations accordingly. You can use a retirement calculator to get a better idea of when you can retire.

Reality Bites: The Retirement Age Cliff

The MassMutual study paints a picture of optimism that doesn't quite jibe with the underlying data. People want to retire at 63, but a significant portion are financially unprepared. Social Security, a crucial safety net, is facing long-term challenges. And the study doesn't offer any concrete solutions or strategies for bridging the gap.

It’s like saying you want to drive a Ferrari, but you only have enough money for a used Corolla. The desire is there, but the resources are… well, not. The discrepancy between aspiration and reality is the real story here.

The data raises some serious questions: How many of these pre-retirees have actually run the numbers and understand the implications of retiring early? How many are factoring in potential healthcare costs, which tend to rise with age? And how many are simply clinging to a romanticized vision of retirement that bears little resemblance to the actual experience?

The Dream vs. the Spreadsheet

I've looked at hundreds of these filings, and the absence of any hard numbers or concrete plans is a glaring red flag. It suggests that many people are approaching retirement with a level of optimism that borders on delusion. Optimism is good, but it's not a substitute for a well-funded 401k and a realistic understanding of your Social Security benefits.

The study is a snapshot of a collective aspiration, but it's also a cautionary tale. It highlights the importance of financial literacy, realistic planning, and a willingness to adjust your expectations in the face of economic realities. Don't let the siren song of 63 lure you onto the rocks.

Retirement at 63? More Like a Financial Gamble

The MassMutual study reveals a dangerous disconnect between retirement dreams and financial realities. It's a reminder that hope is not a strategy, and that a comfortable retirement requires more than just wishful thinking.